NPAs & Bad Banks

Correcting misinformed impressions about NPAs, and the Swedish model for setting up a Bad Bank.

The article was originally published in the Business Standard on February 28, 2018 and re-posted in Organizing India Blogspot on March 1, 2018.

Two features about non-performing assets (NPAs) deserve exploration. First, prevailing impressions about banks and NPAs, such as:

- Large borrowers are primarily responsible for non-performing loans;

- Small borrowers rarely default;

- Privatisation will prevent NPAs and frauds; and

- A bad bank for problem loans will help or it won’t.

Second, solutions for NPAs have been limited to providing some government funding, with hopes of muddling through.First, take the contention that large borrowers account for most bad loans. Of total NPAs of Rs 10,149.16 billion, the published Big 12 comprise 25 per cent (Rs 2,537.29 billion).1 Another 100 wilful defaulters of over Rs 2.5 million against whom suits were filed constitute 7.3 per cent (Rs 740.2 billion).2 While these constitute a third of NPAs, smaller accounts make up the other two-thirds.Among housing loans, NPAs are highest among small loans not exceeding Rs 200,000 (10.4 per cent, or Rs 1,361.26 billion of Rs 13,089 billion), more than double the rate for larger loans over the last five years.3 The lowest NPAs are in the over-Rs 2.5-million category at 0.9 per cent, decreasing with loan size.Housing loans contribute 13.4 per cent to total NPAs, i.e.:

- About half the top 12 defaulters (25 per cent), and

- Double the 100 wilful defaulters (7.3 per cent).

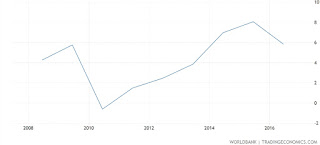

Therefore, the need is for a systemic fix across all levels, not only big defaults.Second, the context for NPAs is the economy. As last year’s Economic Survey (2016-17) pointed out:- A number of NPAs resulted from overleveraging after a high-growth period. Corporates used debt to invest heavily in long-gestation projects in infrastructure, such as power, mines and metals, and spectrum and coal auctions, encouraged by the government. From 2004-05 to 2007-08, the investment-gross domestic product (GDP) ratio rose from 27 per cent to 38 per cent, while bank credit doubled. Then, costs rose along with difficulties in acquiring land and environmental clearances, and oil prices. Import prices rose 2.4 times between 2010 and 2014. The rupee dropped sharply against the dollar, increasing foreign borrowing costs. Domestic borrowing costs also increased with interest rates (Chart 1) as growth fell.

Chart 1: Real Interest Rate: Lending Rate Minus GDP Deflator

https://tradingeconomics.com/india/real-interest-rate-percent-wb-data.html

- By 2013, nearly a third of Indian companies had interest cover less than 1 (EC1), i.e., annual earnings before interest and tax (Ebit) less than interest. By 2015, nearly 40 per cent were at this level. From 2012 through mid-2015, EC1 companies’ earnings were around Rs 250 billion per quarter. By end-2015, earnings had dropped to Rs 20,000 per quarter, and by September 2016, to Rs 15,000 per quarter. Cash flow was insufficient to service debt from 2014. The result was a sharp increase in NPAs (Chart 2), which could increase to 11.1 per cent by September 2018.

Chart 2: NPAs

https://tradingeconomics.com/india/bank-nonperfoming-loans-to-total-gross-loans-percent-wb-data.html

What’s difficult to understand is why and how systemic controls against inappropriate evergreening and fraud, such as integrating SWIFT, or Society for Worldwide Interbank Financial Telecommunication, with in-house systems, and avoiding underreporting of NPAs, have not been enforced until now. Systems have to be properly designed and implemented.However, while we dither over a bank for bad loans, NPAs need resolution. The most salutary model of banking reform, privatisation and recovery is from Sweden.

Sweden’s transformation after its banking crisis of 1991-1992 is remarkable. Their prior experience parallels ours in some ways, although our attributes are very different, i.e., small versus large, advanced/developing, highly skilled small population/underskilled large population, and so on. For years, Sweden was an underperforming economy with low real wage growth, high inflation and public debt. Then a period of rapid growth and credit expansion led to a real estate bubble and collapse, like ours.

Housing prices fell by 25 per cent and commercial real estate by 42 per cent between 1990 and 1995. NPAs went from 5 per cent to nearly 50 per cent among banks (all private), and bankruptcies soared. In this crisis, the entire political leadership decided to unite to resolve their problems. Then, despite fighting behind the scenes, they worked together to take quick action.4 The Swedish centre-right government and the Social Democratic opposition decided on (a) state ownership of troubled banks (b) while guaranteeing all depositors and creditors except bank shareholders.

This united approach restored confidence. A ‘bad bank’ was set up and NPAs evaluated and assigned to ‘good’ or ‘bad’ banks by an independent body disposing of bad assets. Sweden’s banking system recovered to support a sound economy with growth.In our case, undertakings untainted by greed or moral turpitude with cash flow problems deserve efforts at rehabilitation. Examples are where there’s a likelihood of improving cash flows, as in some of the power projects that have run aground for reasons such as lower demand, or exceptional input cost increases. An objective evaluation process by an expert group to triage the NPAs is needed, categorising the untainted and impaired, and where there is scope for revival. Also, rehabilitation measures need to be formulated. The rub is that India is ill-equipped by culture and customary practices to do this. Yet, we would benefit greatly if we could draw on Sweden’s experience in taking corrective action. Private asset reconstruction companies have not been effective. It is unlikely that partial measures will fare better.The primary requirement is political unity across all parties.

Without this, none of the rest can follow. Then, setting up an independent professional entity unencumbered with political considerations to do what is needed. This becomes evident in comparing the US crisis of 2008 (all private banks) with the Swedish experience. After Lehman Brothers collapsed, the Democrats agreed to the Treasury Secretary’s ad hoc $700-billion bailout package, then denounced it just before a vote. The Republicans rejected their own plan, leading to turmoil in the markets. The bill finally passed a week later, and although successful in cleaning impaired assets at a much lower than expected cost, led to a slow recovery and was hugely unpopular. Similarly, the Japanese approach has been slow and not a clear success. Can India’s political parties replicate Sweden’s example? Will they?

Shyam (no space) Ponappa at gmail dot com

1: http://www.business-standard.com/article/finance/steel-firms-dominate-list-of-rbi-s-12-defaulters-117061601393_1.html

2: https://suit.cibil.com/

3:https://rbi.org.in/Scripts/BS_ViewBulletin.aspx?Id=17314

4:http://www.slate.com/articles/news_and_politics/the_pivot/2012/10/sweden_when_its_banks_failed_the_scandinavian_country_made_a_miraculous.html

and

https://www.reuters.com/article/us-sweden-banks-analysis/swedish-banks-safe-bet-or-risky-business-idUSKBN1500ZX

Author

{kind=link}

{kind=link}